Christmas & Tax

With the festive season just around the corner (or already under way), many business owners will be gearing up for year-end celebrations with both employees and clients. Knowing the rules around FBT, GST credits and what is or isn’t tax deductible can help avoid unwelcome surprises on the tax front. Holiday celebrations generally take the form of Christmas parties and/or gift giving.

Parties

Where a party is held on business premises during a working day, is attended by current employees only and comes in at less than $300 a head (GST-inclusive), FBT does not apply, the cost of the function is not tax deductible and GST credits cannot be claimed.

Where the function is held off business premises, say at a restaurant, or is also attended by the employees’ partners, FBT applies where the GST-inclusive cost per head is $300 or more, but not where the cost is below the $300 threshold, as it would be regarded as a minor or infrequent benefit. Where FBT applies, it applies to the entire cost of the event, not just to the excess over $300, while the cost of holding the function is tax deductible and GST credits can be claimed.

Where clients also attend, FBT will not apply to the cost applicable to them (not being employees), but those costs will not be tax deductible and GST credits will not be available.

Gifts

First, you need to work out whether the gift itself is in the nature of entertainment – for example, movie or theatre tickets, admission to sporting events, holiday travel or accommodation vouchers.

Where the recipient of an entertainment gift is an employee, and the GST-inclusive cost is below $300, the minor or infrequent exemption may apply so that FBT is not payable, in which case the cost will not be tax deductible and GST credits are not claimable. For larger entertainment gifts to employees, however, FBT applies, the cost is deductible and GST credits can be claimed.

Where the gift is not in the nature of entertainment and it falls below $300, the FBT minor or infrequent exemption may apply – for example, Christmas hampers, bottles of alcohol, pen sets, gift vouchers.

But because the entertainment rules do not apply, the cost of the gift is tax deductible and GST credits are claimable.

Where a gift is made to a client, the $300 FBT minor benefit exemption falls by the wayside, as long as it is not an entertainment gift and the gift was made in the reasonable expectation of creating goodwill and boosting future sales. Such gifts are uncapped (within reason) and are tax deductible to the business. GST credits are also claimable.

Best approach for employees

Provided it’s not a regular thing, taking employees out for Christmas lunch or dinner escapes FBT, as long as the cost per head stays below the $300 threshold. While the cost of the function will still be non-deductible, that has much less of a cash-flow impact on the business than the grossed-up FBT amounts.

Combined with a non-extravagant off-site

Christmas party, making a non-entertainment gift costing up to $299 is a very tax-effective way of showing your appreciation. Gift cards are always well-received and even where they can be used to make a wide variety of purchases (including theatre tickets and the like), they will not be regarded as an entertainment gift, which means the cost is tax deductible and GST credits can be claimed.

Best approach for clients

While FBT is off the table for business clients, making a non-entertainment gift (tax deductible; no dollar limit) is actually much more tax-effective than wining and dining a key client (non-deductible entertainment). If you put some thought into what gift to buy a client and in some cases deliver it yourself, you may make much more of an impact than joining them in one of many restaurant meals in their already crowded Christmas calendar.

If you need help on the tax treatment of holiday celebrations and gifting, please give us a call.

Deduction for self-education courses

So, you are undertaking a course or further education that relates to your work or business in some way – and you have to pay for the costs of the training or course. Well, the question of whether you can claim a deduction for this cost as “self-education” expenses is not always a clear cut matter.

As a broad proposition, self-education expenses are tax deductible if there is a sufficient connection with your income-producing activities.

In particular, if the expenses are incurred in improving your ability to carry out your current duties, they should be deductible – especially if they are likely to result in a pay rise. By way of a colourful example, the costs of flying lessons for an air traffic controller have been allowed on this basis.

Likewise, a deduction for overseas travel expenses or formal study tour costs incurred by a person may be allowed where the clear purpose of the travel or tour is to increase the specific skills that relate to your job – especially if they may lead to a promotion or pay increase. (But there would always need to be an apportionment for any “private” element of the travel or study tour.)

However, self-education expenses would not be deductible if they were incurred to help you obtain skills for a new occupation.

Nor are they likely to be deductible if they are incurred in a preliminary manner before commencing your new job or a new occupation.

In short, self-education costs will not be deductible if they are undertaken to obtain a new career or obtain new employment.

On the other hand, if you are employed or are self-employed, then the cost of courses or training incurred would be deductible if there is a relevant connection with earning income by way of enabling you to carry out your existing duties better and/ or more skilfully. This could include, for example, undertaking a higher degree that is connected with your current job – and, again, especially if it is likely to lead to increased pay.

Likewise, the expenditure incurred in attending professional development courses and seminars (eg, CPD events) would be deductible (unless these are paid for by your employer).

Similarly, technical books and digital subscription services that improve your knowledge and/or skills in the areas related to your occupation would be deductible – but subject to an apportionment for any “private” usage of the material. For example, an English high school teacher may buy many books which are relevant to his or her job – but there may also be a personal use element.

Which all goes to show that nothing about deductions for self-education expenses is entirely clear cut – so come and see us if you have this issue.

Unwrap your future: 12 super tips for a merry and bright retirement

Christmas is a time for giving, but it’s also a great time to give your future self the gift of financial security. Here are 12 simple superannuation tips to help you make the most of your super fund – wrapped up with a touch of festive cheer!

1. Consolidate your superannuation

If you’ve worked multiple jobs, you might have multiple super accounts. Consolidating them into one fund can save you money on fees, similar to decorating one Christmas tree instead of several. The good news is that consolidating is easy through ATO online services or your myGov account where you can also search for lost or unclaimed super.

Before consolidating, consider potential impacts like the loss of insurance coverage, fees, investment options, and tax implications to ensure the transfer aligns with your needs and adds value.

2. Review your investment strategy

Your super is an investment for your future, so make sure it aligns with your goals and risk tolerance.

Think of it like choosing the perfect star for your Christmas tree – get it right, and it will shine brightly for years. For self managed super funds (SMSFs), it’s a legal requirement to have a documented investment strategy aligned with your objectives, which must be reviewed regularly. Now is a great time to ensure your strategy supports your retirement goals.

3. Check your insurance coverage

Many super funds offer default insurance, including life, total and permanent disablement (TPD), and income protection coverage. It’s essential to review your cover to ensure it provides adequate protection for you and your family. If you manage an SMSF, you’re also required to consider and document the insurance needs of each member as part of the investment strategy.

Seek professional advice to ensure your current cover is sufficient for death, disability or illness.

4. Check your fund’s performance

Not all super funds are created equal, and performance can vary significantly. Regularly check your fund’s performance compared to others to ensure it’s performing. If your fund’s performance is underwhelming, consider revisiting your investment strategy or switching to another fund that better aligns with your retirement goals.

5. Nominate your beneficiaries

Super isn’t automatically part of your estate, so it’s important to nominate valid beneficiaries to ensure your funds go to the right people. Without a valid nomination, your super fund may decide who receives the benefits, regardless of your Will.

Regularly review your beneficiary nominations, especially when circumstances change, to ensure they are up to date and reflect your preference.

6. Make extra contributions

Even small additional contributions can make a big difference to your super balance at retirement thanks to compounding returns. It’s like adding an extra treat to a Christmas stocking – small now, but a delightful surprise in the future. In addition to the 11.5% employer super guarantee contributions for 2024/25, adding extra contributions through salary sacrificing or personal after-tax payments can boost your retirement savings. Just be mindful of contribution caps to avoid extra tax. Small sacrifices now can lead to substantial benefits later.

7. Salary sacrifice

Salary sacrificing is an efficient way to boost your retirement savings and reduce your tax. By redirecting part of your pre-tax salary into your super fund, you can benefit from lower tax rates, allowing more money to work for you in the long term. It’s an easy way to start saving for the future without feeling the pinch today, and over time, compounding returns will help your super grow.

8. Claim your government co-contribution

If you earn below a $60,400 a year and make a voluntary contribution to your super, the government may top up your super with a part co-contribution.

The maximum co-contribution is $500. To receive this maximum amount your income must be below $45,400 and you must contribute at least $1,000 as a personal after-tax contribution into super.

This is a great way to boost your super savings and is a government bonus, much like finding an unexpected gift under the tree.

To be eligible there are several other rules, so check if you qualify and take advantage of this opportunity to grow your retirement savings.

9. Explore spouse contributions

If your spouse earns less than $40,000 pa, you can contribute to their super fund and potentially claim a tax offset of up to $540. This is a great way to help boost their retirement savings and potentially reduce your taxable income in the process.

10. Plan for transition to retirement

If you’re nearing retirement, a transition-to-retirement (TTR) strategy could help you make the most of your savings and ease into retirement more comfortably. This strategy allows you to draw down some of your super while still working part-time, supplementing your income without fully retiring. It’s a way to boost your savings and ensure a smooth transition to retirement, making your golden years as stress-free as possible.

11. Review fees

Super funds charge various fees for managing your money, and these can add up over time, reducing your returns. It’s important to review the fees associated with your super to ensure you’re not overpaying. Much like trimming unnecessary expenses from your Christmas shopping list, minimising fees helps your super balance grow. Check if you’re getting good value for the services provided and whether switching to a more cost-effective option could be beneficial.

12. Seek professional advice

If you’re unsure about any aspect of your super, seeking advice from a financial adviser can be a great step. A financial adviser can provide tailored advice, helping you navigate decisions about your super, investments, and retirement planning. Think of them as your financial Santa’s helpers, ensuring your super journey stays on track and guiding you toward the best financial decisions for your future.

It’s always worth consulting an expert to maximise the benefits of your super and financial planning.

The last word …

By ticking off these 12 tips, you’ll be giving yourself the ultimate Christmas present: a brighter and more secure future. Merry Christmas and happy super planning!

That small farm dream… and tax deductions

Many professionals (and others) who retire – or who are on the verge of retiring – turn their minds to buying farmland and carrying out some sort of small-scale farming activities. And some are already right into it.

But there are some important tax considerations that should be borne in mind in any of those cases – the key one of which is the “non-commercial loss” rules that apply to limit or deny a deduction for losses from that activity.

Importantly, these rules only apply if you are carrying on a business of farming (or any business for that matter) – as opposed to merely “hobby” farming (or any hobby activity). If it is merely a hobby, then generally there are no tax consequences associated with the activity.

However, note that it is not always easy to determine the difference between hobby farming and farming as a business.

But if you are carrying on a farming business (or any business for that matter) the “non-commercial loss” rules will come into play.

And these rules provide that losses from a non-commercial business activity will be restricted from being offset against other income (such as other investment income, rent or salary and wages) unless that business activity satisfies one of the four “commerciality tests”.

Furthermore, if the rules apply, then the non-commercial loss is deferred and, in most cases, can only be offset against profits generated from the same activity in a later year. However, the non-commercial loss rules also do not apply for a farming business if income from other sources is less than $40,000.

So, what are these four “commerciality tests”?

Firstly, if the “income” generated from the business activity is $20,000 or more then the rules will not apply. This includes if it would be estimated that the income would be $20,000 where the activity is only carried on for part of the year. However, there are a lot of rules for how “income” is determined in this case.

Secondly, if the total value of real property used in carrying on the activity is at least $500,000 then again the rules will not apply. But, again, there are a lot of rules for calculating what the value of real property is for these purposes.

Thirdly, if the farming activity resulted in a “profit” in at least three of the past five income years then the rules will not apply.

But, again, there are many rules for how “profit” is determined in this case.

Finally, if the total value of other defined assets used in carrying on the activity is at least $100,000 the rules will not apply.

And just to complicate things, the ATO has a discretion not to apply the non-commercial loss rules if it would be “unreasonable” to do so because the business has been affected by events outside the taxpayer’s control (eg, by drought, flood, bushfire or some other natural disaster).

This discretion can also be exercised where the business is not expected to make a tax profit in the year, but there is an “objective expectation” that it will make a tax profit within some commercially viable period. However, the exact circumstances in which the ATO will exercise the discretion are also governed by various ATO rulings and policy guidelines.

In summary, most of the non-commercial loss rules are fairly straight forward in principle. However, as with any such matters, the devil is always in the detail – and there is a lot of detail attached to these rules.

So, we are here to help you navigate these rules if you are intending to take on a small farming business (or any other business) on your retirement – or if you intend to undertake any business at any time in your working life as the rules apply to any business activity at any stage it is undertaken.

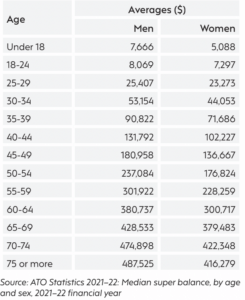

How does your super compare with others your age?

Have you ever wondered how your super balance compares to others in your age group? Or maybe you’re curious about how much you should have saved by now to ensure a comfortable retirement? It’s not always easy to figure out if your super is on track, but understanding how it stacks up can help you make smarter decisions now that will benefit you later. This article looks into the average super balances for people of different ages and explores how much you may need in retirement.

Average balances of Australians

The Australian Taxation Office (ATO) has released data showing average super balances for different age groups. The data gives a helpful overview of where Australians are at in terms of their retirement savings. Here’s how the averages break down:

You might be looking at your super balance right now, feeling either satisfied or a little worried about how it measures up to these averages. Remember, averages don’t tell the whole story. Your balance can be impacted by various factors like career breaks, part-time work, salary levels, or investment decisions.

If you’ve made additional contributions or opted for higher-growth investment options, your balance may be above average. If it’s not quite where you’d like it to be, don’t worry – there’s still plenty of opportunity to take steps and get back on track.

How much super do you need in retirement?

Understanding what you’ll need in retirement can help you gauge whether your super balance is on track.

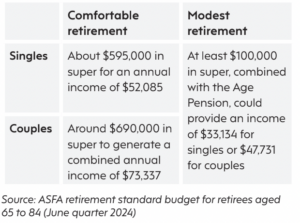

The Association of Superannuation Funds of Australia (ASFA) provides clear benchmarks to define what a “comfortable” or “modest” retirement might look like.

A modest retirement covers basic living expenses, with most of the income coming from the age pension. On the other hand, a comfortable retirement allows for a higher standard of living, including private health insurance, a reliable car, household upgrades, and leisure activities like holidays.

Here’s what ASFA estimates you’ll need if you retire at 65, own your home outright, and are in good health:

Knowing these benchmarks can help you assess your progress and plan for the future you want.

Are you on track?

Now that you know what the average super balance look like, and you have a better idea of how much you may need, it’s time to check where your super stands. If your balance is lower than the targets set by ASFA, don’t panic – it’s never too late to take action.

You can still take steps to boost your super and make it work harder for your retirement.

Consider making extra contributions, whether through salary sacrificing or personal after-tax payments.

Reviewing your investment strategy to ensure it aligns with your goals and risk tolerance is also important. If you’re unsure about what changes to make, it could be helpful to speak to a financial adviser who can offer tailored advice for your situation.

Super is an essential part of your retirement planning, and understanding where you stand can help you make smarter choices today. Whether you’re feeling confident about your balance or realising there’s more work to be done, it’s always worth taking the time to review and plan ahead. The sooner you act, the more time your super will have to grow – putting you in a better position to enjoy your golden years.

Click to view our Glance Consultants December 2024 Newsletter via PDF